Calculate credit risk and value at risk: the indispensable tool for banks.

Credit Risk Evaluator

Credit risk management, more transparent than ever before.

The Credit Risk Evaluator provides and reports risk and return analyses at all portfolio levels - from individual clients to the entire portfolio. It thus creates the basis for reliable results and provides suggestions for concrete actions in sales and management. This applies to the entire credit risk management. The tool's handling is convincing due to its extraordinary conception as an open library of credit portfolio models. Currently, the standard package includes seven models, which are available to you at the click of a mouse. In this way, you can easily see how the respective model affects your risk - and, if necessary, initiate appropriate measures. Discover "The Library of Credit Portfolio Management"!

Advantages

- Full transparency for bank-wide credit risks

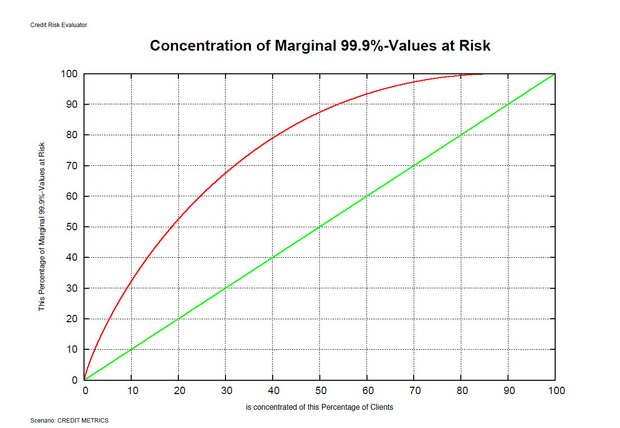

- 7 different credit models, including CreditMetrics and CreditRisk+, to highlight portfolio strengths and weaknesses

- New standards in risk and return analysis, automation, performance and user-friendliness

- Assessment of risks and returns at client, segment and portfolio level

- Targeted identification of improvement potential

- Strategic analyses and integration of country risks

- Coverage of Basel 2 and the possibility of further leveraging investments

- Maximum recovery uncertainty analysis

- Simple implementation, batch processing of scenarios and fast computing power